Trucking Industry 2026 Outlook

April 2026

Updated April 30, 2026

Trucking Industry Forecast 2026: Market Conditions Improve in April

The trucking industry enters April 2026 in a stronger position than it held a year ago. While the market is not yet in a full expansion cycle, conditions continue to improve as excess capacity exits the system, freight pricing strengthens, and equipment demand becomes more constructive.

The environment remains defined by transition rather than acceleration. Freight demand is still uneven across sectors, but tightening driver availability, firmer spot and contract rates, and improving supply-demand balance are creating a healthier operating backdrop for fleets, carriers, dealers, lenders, and industry decision-makers.

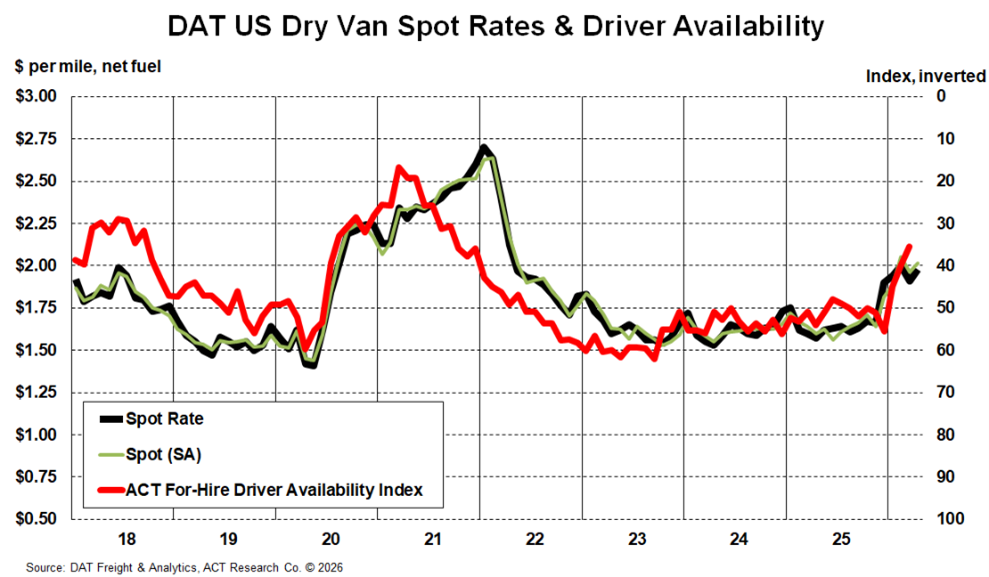

Freight Markets Continue to Rebalance

One of the most important developments in 2026 is the continued recovery in freight market fundamentals.

Spot truckload activity has remained above prior-year levels, rate conditions have improved, and contract pricing is beginning to respond as market capacity tightens. While freight demand is not uniformly strong across every sector, pricing trends suggest the market has moved materially beyond the weakest conditions of the prior cycle.

For carriers and transportation buyers, this shift matters because stronger pricing typically improves fleet profitability, replacement confidence, and capital planning visibility.

Capacity Tightening Is Reshaping the Market

The recovery is being supported not only by demand, but also by reduced supply.

After several years of oversupply across trucks and drivers, the market is tightening. Carrier exits, slower fleet expansion, and growing driver constraints are limiting available capacity and helping accelerate rebalancing across the industry.

This creates a different type of recovery than prior cycles. Rather than relying solely on a freight demand surge, 2026 is increasingly being shaped by structural tightening that supports rates and restores healthier market discipline.

Truck and Trailer Markets Show Mixed but Improving Trends

Equipment markets are improving, though not all segments are moving at the same pace.

Class 8 demand has strengthened meaningfully as fleets respond to better freight conditions, replacement needs, and upcoming regulatory changes. Medium-duty markets remain softer and more tied to housing and small-business activity. Trailer demand continues to stabilize, with sentiment improving gradually alongside freight market recovery.

For buyers, the takeaway is that planning decisions may increasingly vary by equipment class, application, and replacement timing rather than following one broad industry trend.

EPA 2027 and Cost Pressures Are Influencing Decisions

Regulatory timing remains one of the most important strategic forces shaping 2026.

As fleets prepare for EPA 2027 emissions requirements, many are reassessing purchase timing, replacement schedules, and future equipment costs. At the same time, higher fuel prices, financing costs, insurance expense, and tariff-related pricing pressure continue to influence capital allocation decisions.

That combination is encouraging many operators to stay disciplined while still preparing for future demand needs.

Used Truck Markets Add Another Positive Signal

The used truck market has also improved, adding support to the broader industry outlook.

Sales activity has strengthened and pricing trends have stabilized compared with prior-year conditions. A healthier secondary market can improve trade values, replacement flexibility, and confidence for fleets evaluating new equipment purchases.

This does not mean all challenges have disappeared, but it is another sign that industry conditions are stronger than they were during the downturn.

Trucking Industry Forecast 2026: Bottom Line

The trucking industry continues to move in a healthier direction in April 2026.

Freight pricing is improving, capacity is tightening, equipment demand is becoming more constructive, and regulatory timing is influencing fleet decisions. While the recovery may remain gradual and uneven across sectors, the market has clearly improved from the conditions that defined the previous two years.

For fleets, buyers, suppliers, dealers, and investors, 2026 is increasingly becoming a year of better planning visibility and stronger strategic opportunity.

Stay Ahead with Smarter Freight Insights

Success in trucking and freight comes from knowing what’s next—not just what’s now. At ACT Research, we deliver forward-looking market intelligence that helps you anticipate shifts, prepare for cycles, and stay strategically positioned. As your trusted transportation intelligence partner, we give you the tools to act with confidence—so you can optimize operations, reduce risk, and drive stronger profitability.