According to this month’s issue of ACT Research’s State of the Industry: U.S. Trailers report, four months into 2026 and the US trailer industry remains mired in the same challenging environment in which it operated throughout 2025.

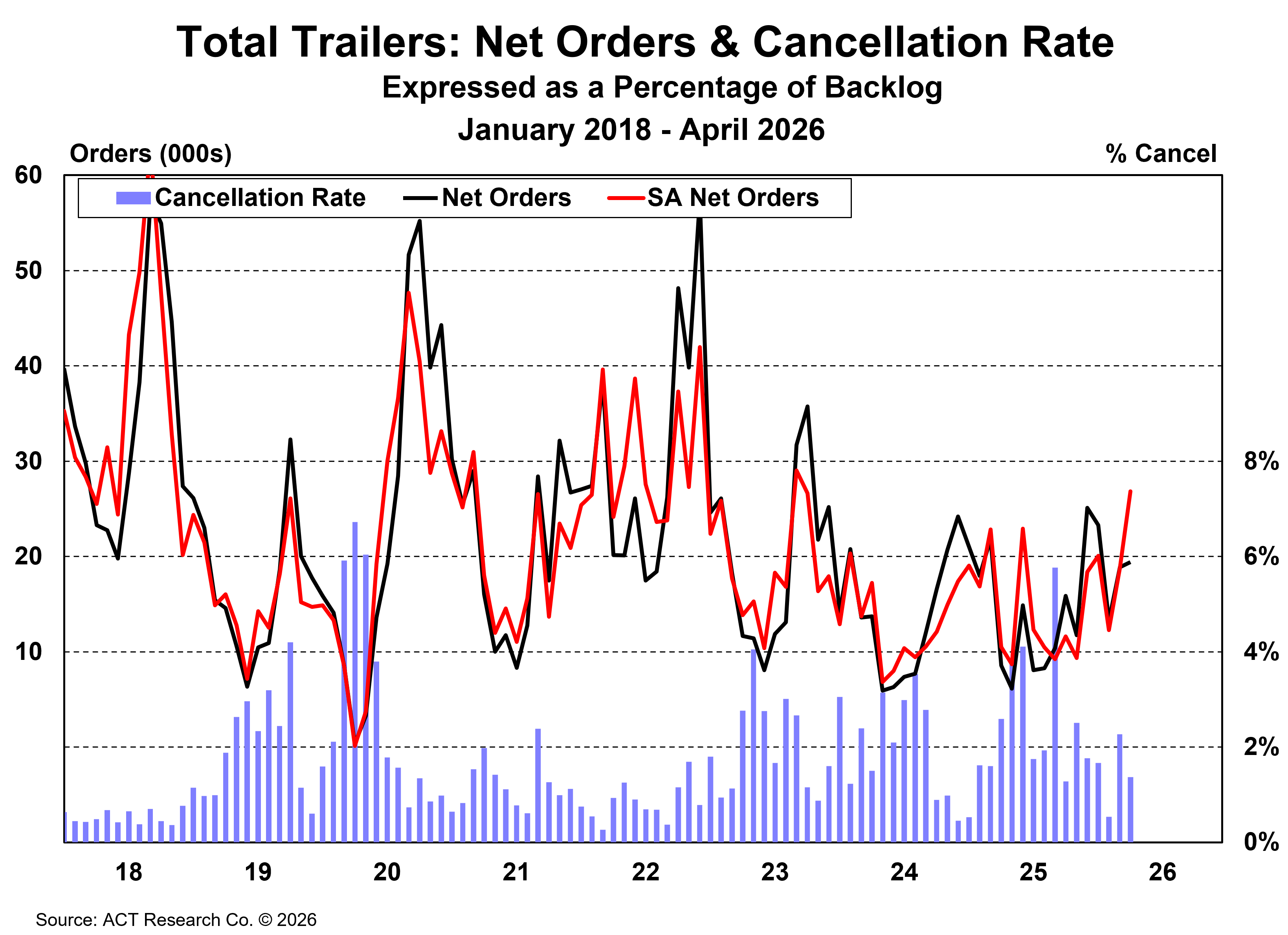

“Counter to cyclical expectations, net order intake in April increased from March, albeit by just 3%, logging 19.4k orders placed this month. Compared to April 2025, net orders vaulted nearly 127% over the subdued intake of 8.6k last year. Seasonally adjusted, trailer orders were 26.8k units compared to an 18.8k SA rate in March, up almost 43% m/m,” said Jennifer McNealy, Director–CV Market Research & Publications at ACT Research. “April’s cancellation rate of 1.4%, as a percentage of backlog, remained in ‘elevated’ territory, but was an improvement from the 2.3% rate recorded in March. Like last month, high cancellations were reported in most segments, meaning the situation was broad-based.”

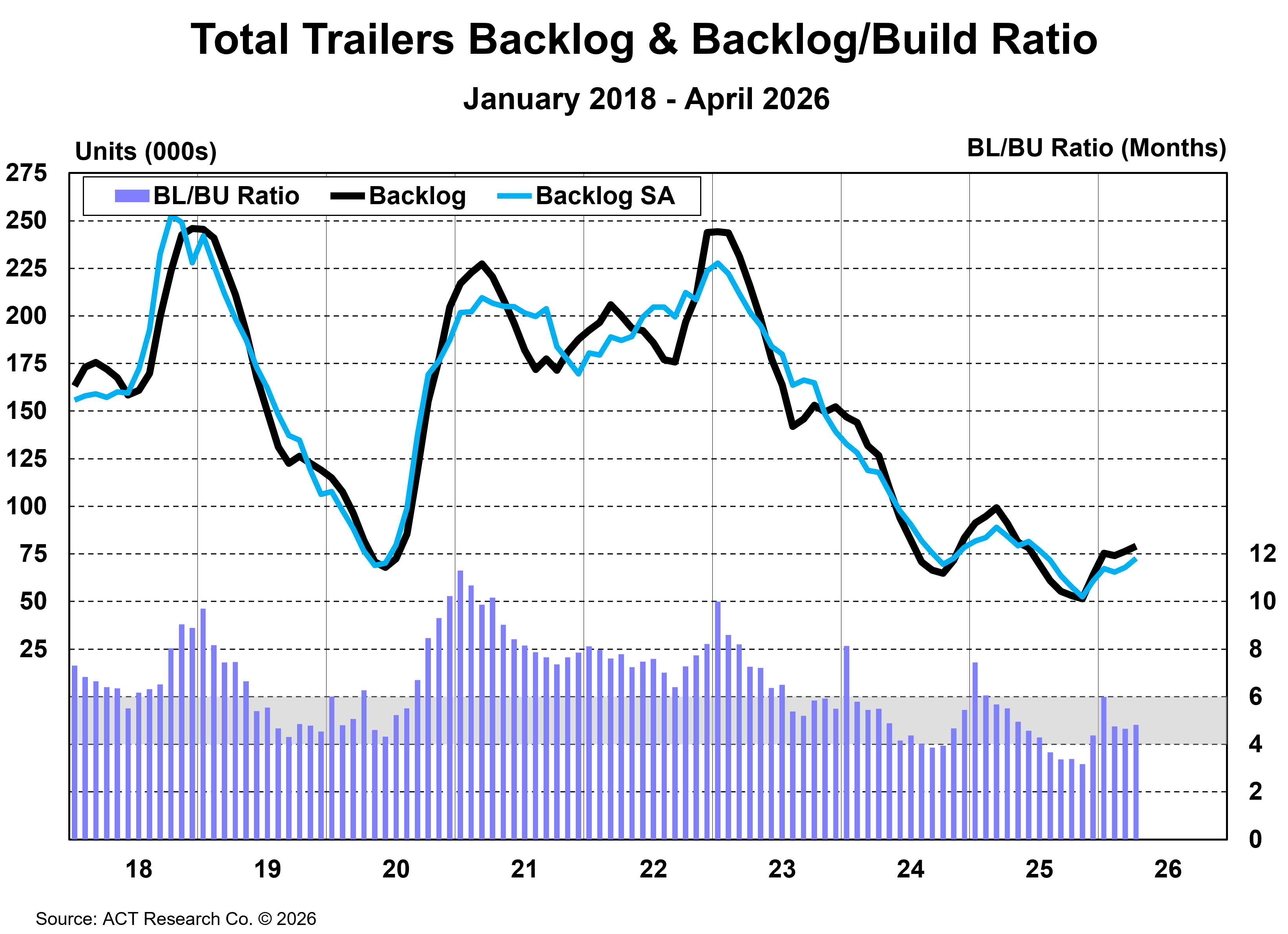

“Net orders have outpaced build for three of the four months in 2026. In April, nearly 2.3k more trailers were ordered than built, growing the backlog by more than 3% m/m,” McNealy continued. “However, this was not enough to pump much lifeblood into the anemic backlogs. YTD, backlogs contracted more than 13% compared to the first trimester of 2025.”

State of the Industry: U.S. Trailers Report Overview

ACT Research’s State of the Industry: U.S. Trailers report provides a monthly review of the current US trailer market statistics, as well as trailer OEM build plans and market indicators divided by all major trailer types, including backlogs, build, inventory, new orders, cancellations, net orders, and factory shipments. It is accompanied by a database that gives historical information from 1996 to the present, as well as a ready-to-use graph packet, to allow organizations in the trailer production supply chain, and those following the investment value of trailers, trailer OEMs, and suppliers to better understand the market.

ACT Research Overview

ACT Research is recognized as the leading publisher of commercial vehicle truck, trailer, and bus industry data, market analysis, and forecasts for the North America and China markets. ACT’s analytical services are used by all major North American truck and trailer manufacturers and their suppliers, as well as banking and investment companies. ACT Research is a contributor to the Blue Chip Economic Indicators and a member of the Wall Street Journal Economic Forecast Panel. ACT Research executives have received peer recognition, including election to the Board of Directors of the National Association for Business Economics, appointment as Consulting Economist to the National Private Truck Council, and the Lawrence R. Klein Award for Blue Chip Economic Indicators’ Most Accurate Economic Forecast over a four-year period. ACT Research senior staff members have earned accolades including Chicago Federal Reserve Automotive Outlook Symposium Best Overall Forecast, Wall Street Journal Top Economic Outlook, and USA Today Top 10 Economic Forecasters. More information can be found at www.actresearch.net.

Additional Resources

Preliminary net trailer orders in April were 19,400 units. While April orders were up only about 600 units from March’s 18,800-unit level, a 3% month-to-month increase, they vaulted over the tepid showing in April 2025, up 126% y/y. Seasonal adjustment (SA) at this point in the annual order cycle takes the month’s volume to 26,800 units. Final April trailer industry data will be available later this month. This preliminary order estimate is typically within ±5% of the final order tally.

“A sequential drop in net orders is typically expected, as April traditionally marks the second consecutive month of ‘weakest’ months of the annual order cycle,” said Jennifer McNealy, Director CV Market Research & Publications at ACT Research. “That said, this year’s cycle seems to have been delayed a few months, as the order upticks that should have started in September or October of last year didn’t actually happen until December. Regardless of the timing, the order upticks certainly are welcome.”

McNealy concluded, “Given accelerating freight rates and rising carrier confidence, we raised the question last month about whether more high-side surprising order intake months would happen, or whether traditional Q2 order weakness would prevail as fleet decision-makers continue to hesitate about placing trailer orders while accelerating Class 8 tractor purchases instead in 2026. Based on the April data, we now know there was at least one more month of improved order intake in the pipeline, but it remains to be seen how the final two months of Q2 will unfold. Additionally, concern is mounting about how quickly trailer OEMs will build down the relatively still-thin backlog, particularly given concerns about the level of activity in the key freight-generating economic sectors that drive transportation demand and high petroleum prices that weigh on purchasing decisions for both consumers and fleets.”

- Cancellation Rate as a % of Backlog: 1.4%

- Backlogs: grew 3% m/m

Click here to learn more information about ACT's Mexican Trailer Market report.

ACT Research is featured regularly by major news outlets for our work covering Class 8 truck orders, sales, forecasting, used truck sales, freight rates, trailer sales, and much more. Get more trends, HERE.

Save time with ACT Research’s media kit. Access ACT Research’s analyst bio, logos, press releases, video library, and more at your convenience. Our analysts are committed to delivering the most accurate data and forecasts. Looking for a speaker? Each analyst is available to speak at your conference or event. Access Media Kit Here.